How Investors Quickly Eliminate Bad Rental Deals Using Rent-to-Price Ratios

When you're looking at dozens of listings a week, you can't run a full cash flow model on each one. You need a first-pass filter that kills the obvious losers in seconds. The rent-to-price ratio is that filter.

It won't tell you if a deal is good. It will tell you, fast, which deals aren't worth a second look, so you spend your modeling time where it counts.

What the rent-to-price ratio is

The ratio compares expected monthly rent to purchase price, as a percentage:

Monthly rent ÷ purchase price = rent-to-price ratio

A property renting for $1,800 at a $240,000 price gives $1,800 ÷ $240,000 = 0.75%. That single number tells you how efficiently the property turns price into rent before any costs.

Why investors screen with it first

Speed. One division flags a weak deal instantly. No spreadsheet required.

Consistency. The same ratio compares cleanly across markets and price points.

Scale. You can run it on a hundred listings in the time a full model takes for one.

If a property fails this test, it almost never recovers once expenses, financing, and vacancy come out. The ratio is a triage tool, not a verdict.

Common benchmarks

| Rent-to-price ratio | What it usually means |

|---|---|

| 0.5% or less | Unattractive unless you're betting on appreciation |

| 0.6% – 0.8% | Borderline; only worth modeling if other factors are strong |

| 0.9% – 1.0% | Solid starting point for cash-flow investors |

| 1.1%+ | Rare, often attractive if the rent is realistic |

Benchmarks shift by market, but the bands hold: low ratios rarely turn into cash flow.

A worked example: screening four deals at once

Say you pull four listings in the same metro and estimate market rent for each. Here's the triage, against a 0.8% minimum:

| Property | Price | Est. rent | Ratio | Verdict |

|---|---|---|---|---|

| A | $250,000 | $2,300 | 0.92% | Advance |

| B | $400,000 | $2,600 | 0.65% | Discard |

| C | $180,000 | $1,650 | 0.92% | Advance |

| D | $320,000 | $2,050 | 0.64% | Discard |

Two of four are gone in under a minute. You now run full cash flow only on A and C. That's the entire point: spend modeling time on the deals that can survive it.

The ratio is only as good as the rent

Here's the trap. The price in the formula is fixed by the listing, but the rent is an estimate. Overestimate rent by 10% and a 0.65% deal looks like 0.72%. Suddenly a discard becomes a "maybe," and you waste an afternoon on it.

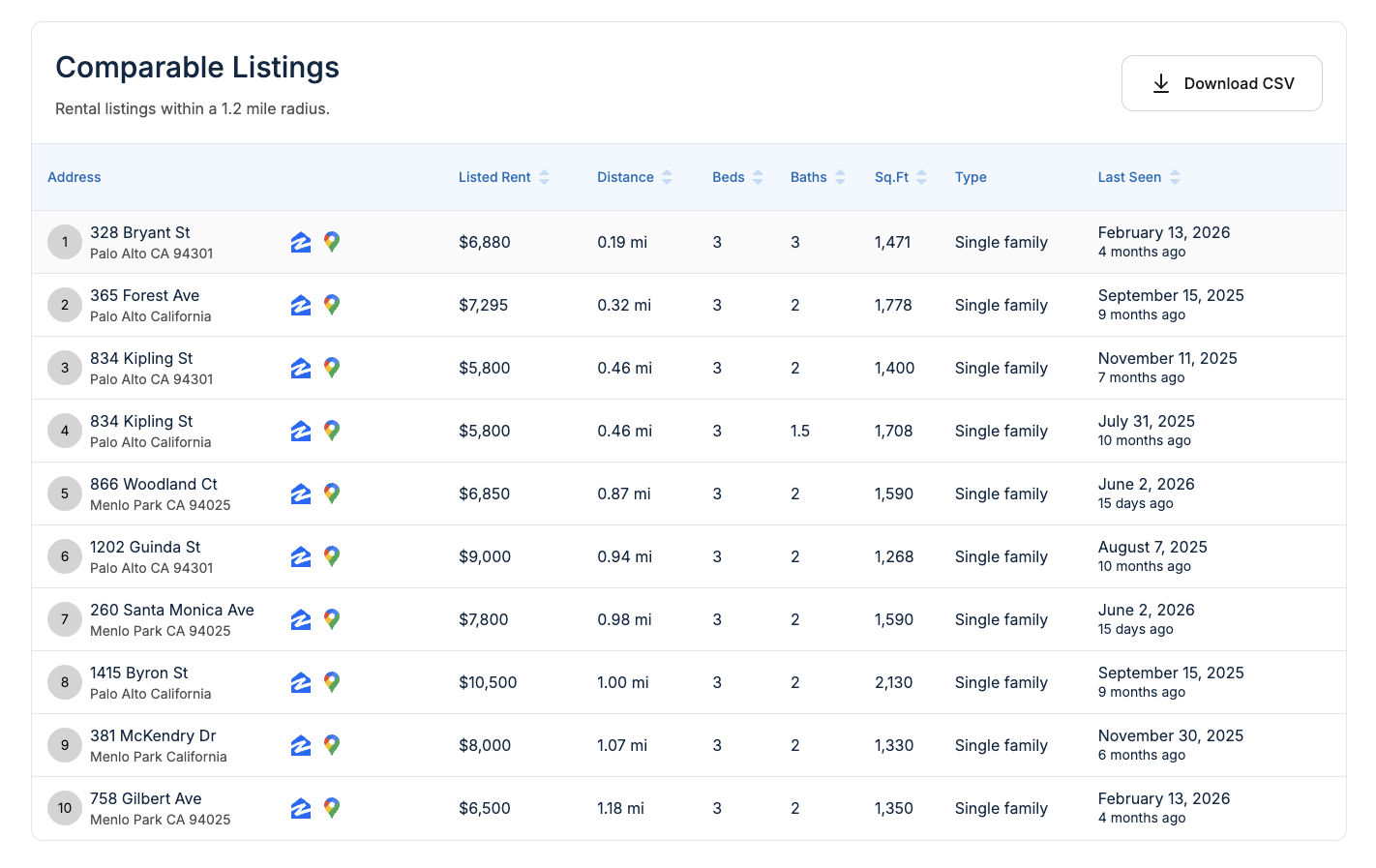

So the rent figure has to come from real local comps, not a hopeful round number. Pull a rent estimate by address and look at the comps behind it before you trust the ratio.

When you're scanning a whole area rather than one address, a rent estimate by zip code helps you spot neighborhoods where ratios tend to clear your threshold.

What the ratio doesn't tell you

The filter is deliberately blunt. It ignores:

- Operating expenses and property taxes

- Insurance and maintenance

- Vacancy and turnover

- Financing terms and leverage

That's why it's a screen, not a decision. A property that passes still has to survive a full model.

After it passes the filter

Once a deal clears the ratio, the real analysis starts:

- Cash flow and cap rate with every expense line

- Expense modeling adjusted for property age and condition

- Detailed comp review to confirm the rent holds up

- Exporting data for your underwriting model

Comps you can download to CSV, plus the full comparable table behind each estimate, make that next stage faster.

The takeaway

The rent-to-price ratio is the cheapest filter in real estate. One division eliminates the deals that can't work, so your spreadsheet time goes only to the ones that can. Just make sure the rent in the numerator is real, because an inflated estimate is the one thing that makes the filter lie.

Run a rent estimate by address and let real comps set the rent before you screen.

Frequently asked questions

What is a good rent-to-price ratio for rentals? Many investors target at least 0.8%–1.0%, though acceptable ratios vary by market and strategy.

Is the 1% rule still realistic? In many markets the classic 1% rule is rare, but ratios below it can still work depending on expenses and financing.

Can rent-to-price ratios replace cash flow analysis? No. They're a screening tool, not full underwriting.

Should I use asking price or purchase price? Use the realistic purchase price you expect after negotiation, not the list price.

Do rent-to-price ratios work for multifamily? Yes, but they're most common for single-family and small multifamily deals.

How do I calculate this quickly for many properties? Bulk rent estimates or zip-level rent data let you scan many deals at once.