What a 10% Rent Error Really Costs Over a 5-Year Hold

Investors obsess over purchase price, renovation budgets, and exit cap rates. The most common underwriting mistake is simpler and quieter: being wrong on rent.

A 10% rent error doesn't sound dramatic. If market rent is $2,000 and your model assumes $2,200, that's $200 a month. But over a five-year hold, that small miss compounds into real cash flow loss, a lower sale price, and sometimes a deal that never should have closed.

This post puts a dollar figure on it.

Why a 10% rent error is more dangerous than it sounds

Rent drives nearly every downstream number in a rental deal:

- Monthly cash flow

- Debt service coverage ratio (DSCR)

- Cash-on-cash return

- Exit valuation, through NOI

When the rent input is wrong, everything built on top of it is wrong too. The error doesn't stay contained, it cascades.

Baseline: a reasonable-looking deal

Start with a conservative, common scenario.

| Assumption | Value |

|---|---|

| Purchase price | $300,000 |

| Expected market rent | $2,000 / month |

| Operating expenses | 35% of rent |

| Annual rent growth | 3% |

| Hold period | 5 years |

Now watch what happens when the rent is off by 10%.

The 10% overestimate

Instead of $2,000/month, the model assumes $2,200. That's $200 a month, or $2,400 a year, of rent that isn't really there.

Year one impact. Gross rent shortfall is $2,400. After 35% expenses, the net operating income shortfall is about $1,560. Your expected cash flow is already off by more than $1,500 in the first year alone.

Five-year cumulative loss. Apply 3% growth to the wrong base and the missed NOI compounds:

| Year | Missed NOI |

|---|---|

| Year 1 | $1,560 |

| Year 2 | $1,607 |

| Year 3 | $1,655 |

| Year 4 | $1,705 |

| Year 5 | $1,756 |

Total missed NOI over 5 years: about $8,283.

The exit hit most investors miss

The bigger damage shows up at sale. Income properties are valued on NOI. If your actual NOI is lower than projected, your exit price drops even if cap rates never move.

At a 6% exit cap, the year-five NOI shortfall alone reduces value by:

$1,756 ÷ 0.06 = about $29,000

That's the sale-price hit from the rent error, on top of the cash flow you already lost.

Total cost of a 10% rent error:

- Missed cash flow: about $8,300

- Reduced exit value: about $29,000

- Combined impact over a 5-year hold: about $37,000

A $200/month assumption became a five-figure decision.

Why it happens so often

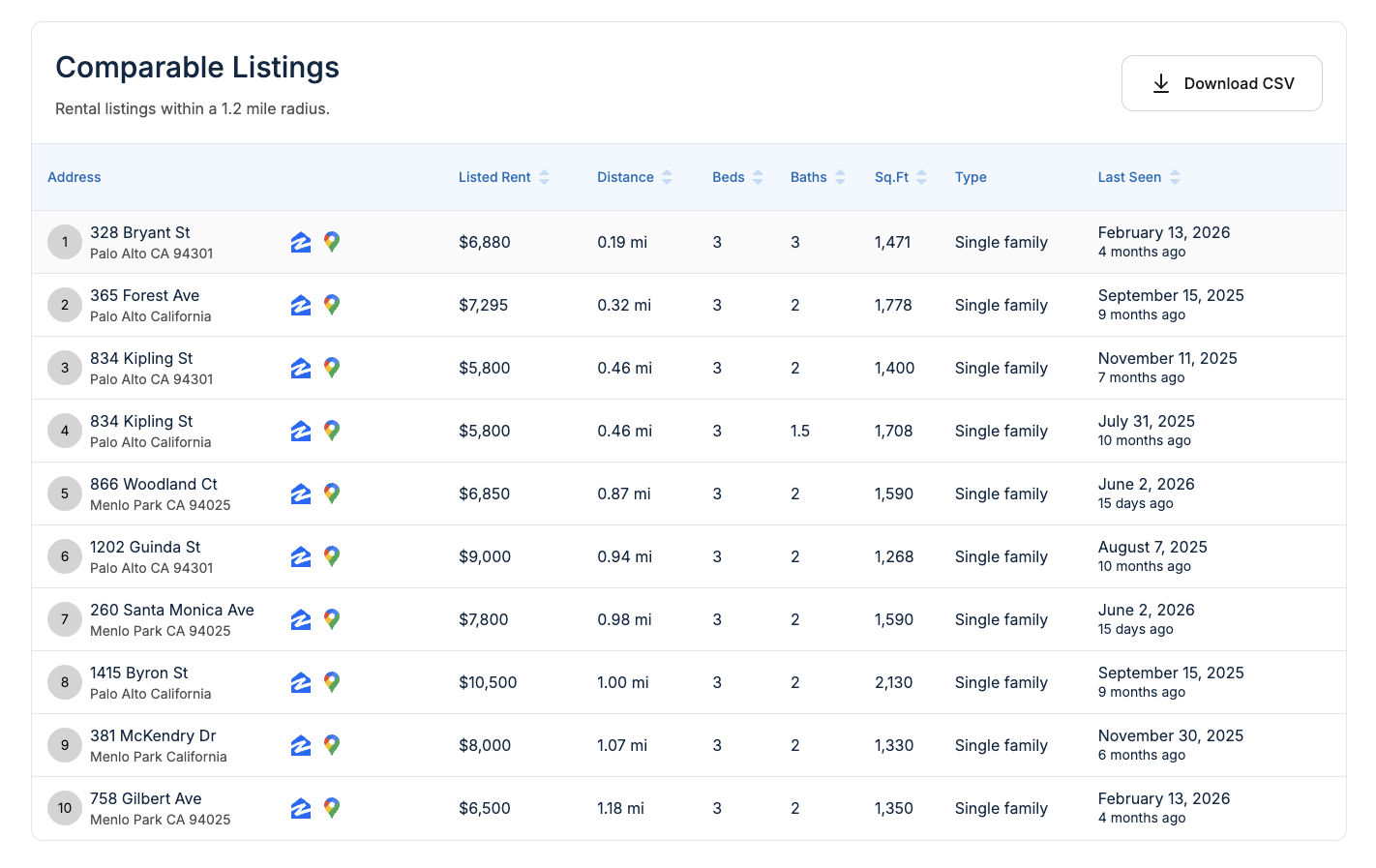

Rent errors rarely come from bad arithmetic. They come from bad comps:

- Using listing rents instead of leased rents

- Mixing apartments with single-family homes

- Pulling comps from too wide a radius

- Ignoring age or condition differences

- Trusting a free estimate without checking what's behind it

This is why disciplined investors validate the rent before they trust any return metric.

A simple framework to avoid overestimation

- Start with a rent estimate by address, not a zip-wide average.

- Confirm comps match the unit type, single-family with single-family.

- Read the median, not just the average.

- Check how many comps the estimate used; more isn't always better.

- Stress-test returns at 5–10% below your projected rent.

The fastest way to catch a bad number is to look at the comparable listings behind it.

If the comps are stale, far away, or the wrong type, the rent figure is shaky, and so is the $37,000 riding on it.

Why ratio screeners catch this early

Investors who screen with rent-to-price ratios often spot rent errors fast. If a deal looks great on paper but the ratio weakens once you validate rent with better comps, that gap is the warning. Tools that expose comp quality, historical rents, and realistic ranges make the mistake visible before capital goes in.

The takeaway

A 10% rent error isn't a rounding mistake. It's a five-figure decision error that hides inside an innocent-looking $200. Before you argue about renovation budgets or refinance timing, make sure the rent number holding up the entire model is defensible.

Pressure-test it before you buy. Run a rent estimate by address and ground your projection in real, local comps.

Frequently asked questions

Is a 10% rent error common? Yes. In markets with thin data or fast-changing conditions, 5–15% variance is common with listing-based or generic estimates.

Does this apply to short holds? Even on a 1–2 year hold, a rent error can break DSCR or erase expected cash flow, especially with leverage.

Is underestimating rent just as bad? It's less risky financially, but it can make you pass on viable deals. Overestimation is the more dangerous direction.

How often should rent assumptions be updated? At acquisition, before refinancing, and annually for long-term holds, especially in volatile markets.

Do free rent estimates cause this? They can. Free tools are fine for rough screening, but relying on them without comp validation raises error risk.